Ta StrategyHello guys

This script follows traditional technical indicators

MACD, ADX, RSI and pivot points

If the price is above the resistance and the MACD has crossover ,and the RSI 14 is above 50

ADX is higher than 20, and DI+ is higher than DI-. This is a buy signal and vice versa for a sell signal

The script moves the stop loss to the entry price after the first target is reached

You can specify the quantity you want to sell when the price reaches the first target

There are also options like if you want the script to entry long or short, or both

you can reverse the strategy if it does not work well

If you want to inquire about any details, please let me know in the comments

"the script" için komut dosyalarını ara

The Z-score The Z-score, also known as the standard score, is a statistical measurement that describes a value's relationship to the mean of a group of values. It's measured in terms of standard deviations from the mean. If a Z-score is 0, it indicates that the data point's score is identical to the mean score. Z-scores may be positive or negative, with a positive value indicating the score is above the mean and a negative score indicating it is below the mean.

The concept of Z-score was introduced by statistician Carl Friedrich Gauss as part of his "method of the least squares," which was an important step in the development of the normal distribution and Z-score tables. It's a key concept in statistics and is used in various statistical tests.

In financial analysis, Z-scores are used to determine whether a data point is usual or unusual. You can think of it as a measure of how many standard deviations an element is from the mean. For instance, a Z-score of 1.0 would denote a value that is one standard deviation from the mean. Z-scores are also used to predict probabilities, with Z-scores having a distribution that is expected to be normal.

In trading, a Z-score is used to determine how often a trading system may produce a string of winners or losers. It can help a trader to understand whether the losses or profits they see are something that the system would most likely produce, or if it's a once in a blue moon situation. This helps traders make decisions about when to start or stop a system.

I just wanted to play a bit with the Z-score I guess.

Feel free to share your findings if you discover additional applications for this strategy or identify timeframes where it appears to perform more optimally.

How it works:

This strategy is based on a statistical concept called Z-score, which measures the number of standard deviations a data point is from the mean. In other words, it helps determine how unusual or usual a data point is.

In the context of this strategy, Z-score is applied to a 10-period EMA (Exponential Moving Average) of Heikin-Ashi candlestick close prices. The Z-score is calculated over a look-back period of 25 bars.

The EMA of the Z-score is then calculated over a 20-bar period, and the upper and lower thresholds (bounds for buy and sell signals) are defined using the 90th and 10th percentiles of this EMA score.

Long positions are taken when the Z-score crosses above the lower threshold or crosses above the mid-line (50th percentile). An additional long entry is made when the Z-score crosses above the highest value the EMA has been in the past 100 periods.

Short positions are initiated when the EMA crosses below the upper threshold, lower threshold or the highest value the EMA has been in the past 100 periods.

Positions are closed when opposing entry conditions are met, for example, a long position is closed when the short entry condition is true, and vice versa.

Set your desired start date for the strategy. This can be modified in the timestamp("YYYY MM DD") function at the top of the script.

Gold Fair Value Gap Entry(FVG GOLD)This script calculates the fair value of gold, which is set as an input parameter. It then gets the current price of gold and calculates the gap between the price and the fair value. If the gap is positive, it enters a long trade, and if it's negative, it enters a short trade.

The script also uses proper risk management techniques by setting a stop loss and take profit for each trade. The plot() function is used to display the fair value and gap on the chart.

Please note that this is just an example script, and you should customize it based on your specific trading strategy and criteria. It's also important to backtest your strategy and refine it before using it with real money.

[SPOILED]SuperTrench - ETH Super ScalperHi Traders,

I'm republishing this script as I finally polished it to perfection IMO. The script uses 5 coding sections: entry, trend filter, pivot filter, take profit, and stop loss. The script mainly uses trailing as take profit; this is probably the easiest way to make a profitable scalper strategy.

Backtest capital is set to 1000 USDT, 35% equity, 0.04% commission, limited backtest date from Jan 2022 to now, backtested on ETH/USDT prep contracts 15m timeframe, result as shown below.

It looks unreal right? Hell no, I actually tested this strategy on Binance from Dec 06 to Dec 10. I got 8.29% return with 4x leverage, 50% equity setup; 75% win rate,1.58 profit factor, with 4.3% max drawdown, it is amazingly close to the backtest result.

User Manual

Entry >>> Stoch RSI:

I added 5 MA types to the Stoch RSI which is HMA/VWMA/WMA/EMA/SMA, HMA with Length setting of 5, 8 seems to be most efficient, VWMA and WMA with 8, 13 will generate less entry signals but with less entry risks.

Entry >>> R Style:

It based on price action, with candlestick makes a U turn, after 2nd candlestick confirmed, it generates entry signal, this will give you some extra entries, better leave it enabled.

Entry >>> Price Step:

This probably is the core feature of this strategy; also my secret ingredient to making this strategy this efficient. It is recommended to enable step 1-5, more steps basically means more entries, but they are not necessarily profitable.

Trend Filter >>> Price Step:

I couldn't tell you much details about how this indicator works, but it is a reliable indicator, based on price action, and I got some ideas from Demark9 indicator. The bigger the level, the stronger the filter is, please note that if 'Price Step Entries' less than Price Step Trend, entries will be ignored.

Pivot Filter >>> RSI Pivot & Pinbar Pivot:

RSI Pivot detects if the RSI signal line making U turn in certain condition, Pinbar detection combines R Style entry when price action U turn took place, these 2 pivot filter will close the trade once it is counter trend, so it better enable and leave it as is.

Trend Filter >>> Trend Magic:

Trend Magic uses CCI and ATR to calculate trend status, green means uptrend, red means downtrend, pretty straight forward, the best value for this indicator would be, 21, 34, 55, 89.

Trend Filter >>> Alpha:

This filter combines R style pivot, price step, EMA all together to detects consolidation area, because EMA was involved, so the best look back period would be around 15-35, it is best to use default value IMO, in another hands, if you need stronger filter, feel free to use 10, 18, 20, 25, 30, 35, make sure look back period should increase or decrease by 5 every time.

Take Profit and Stop Loss:

The default value for tp is set to 0.4%, but I also give you option to switch to ATR TP; you can adjust in the ATR multiplier, default ATR trailing stop loss uses 1 ATR, but you can adjust it for better drawdown tolerance. Fixed ATR SL is also given when fixed ATR is enabled. There will be a failsafe SL default set to 1% if price moves counter direction of opened position, it will close trade no matter what happens.

Enjoy :)

Wunder DCA BotThe bot is based on the DCA system.

1. DCA is the investment method in which you buy a certain portion of the asset after the determined price deviation.

2. For entry, we evaluate the maximum and minimum levels for a given period that you can adjust in the script. The bot enters when price rebound from the specified levels.

3. For the exit, the bot will use the take profit percentage that you will specify in settings.

It is also possible to choose how the take profit is calculated either from the average entry price or from the entry order (first order).

4. DCA uses the following settings:

- Base order Volume: Volume of your first order on entry signal

- Subsequent orders volume: The volume of all subsequent orders except the first

- DCA orders count: This parameter will determine how many entries your overall strategy will have. For example: If you will put 3, that will mean that including your initial position you will have 2 additional orders.

- DCA order price deviation:

This is the value in % which determines the deviation of the additional entries from the entry price. Example: If you go long and the price of the asset is 100$ and you put an order price deviation of 1% that will mean that the first additional entry will occur when the price will drop by 1%, and the second entry will be triggered when the overall price will drop by 2% (as the interval between the first and the second additional entry will be 1%).

- DCA Order Volume Multiplier:

This parameter will determine the amount that you put into each additional position. If this parameter is equal to 1 that means that each additional entry will be equal to the initial amount. The extra volume will be added to your position from the second DCA entry. Example: Your initial position was 10$ and your Volume Multiplier is set to 2. When you reach your 1st DCA target your additional order will have the same volume of 10$. When you reach your 2nd DCA target your additional order will be 20$ (previous position volume * multiplier). Your 3rd DCA target will place the order of 40$.

- DCA order price Deviation Multiplier:

This value will increase the price deviation between each additional entry. It is calculated as the price deviation multiplied by the deviation multiplier. For example: if you enter long at the price 100$ and have a price deviation of 1% with the price deviation multiplier of 2 that will mean that the first additional entry will occur when the price will drop to 99$ however the second will occur when the price will go to 97$. The third additional position will be entered at 94$

5. For full automation of the bot, you should set your comments to the input in the bot settings in the "LONG" and "SHORT" fields. You also need to create an alert signal and set a Webhook to send signals.

IMPORTANT!!!

1. Position calculation should take into account several factors: your deposit, leverage, the number of DCA orders, the distance to the last DCA order;

2. When choosing leverage, it is important to correctly calculate the possible drawdown. If you set a high leverage value, then liquidation awaits and the bot will not be able to take profits and will exit the position ahead of time;

3. The size of the position must be determined in accordance with all risks and take into account the size of your deposit;

4. This DCA Bot is able to earn consistently with the correct calculated money management.

Plutus - StrategyPlutus is a Script I've been working on for the past several months, and It's finally ready to go live! I would like to have few volunteers to help me forward-test it with different assets, preferably, with any Binance Perpetual contract traded under US$50.

The Script is delivering a Net PnL of circa 350% (0.04% commission deducted from the ~500% gross) in 14 days on the backtest when plotted on the WAVESUSDTPERP 2-min chart. Good results also with RUNEUSDTPERP and OGNUSDTPERP .

To whomever contributes with a constructive (technical) feedback, a better Stop-Loss strategy, other potential (Binance Futures ) pairs where the Script would delivery a 15-Day PnL of 400%+, and MAINLY who collaborate fowardtesting it, I'll grant access to the Strategy (which will have its Privacy Setting changed from Public to Private in 7 days from now) for a period of 2 months.

Please, explored it with different time frames, assets, markets and leave your comments!

Thanks a lot!

PS.: Tomorrow I'll write a better description.

Trendelicious StrategyA simple strategy based on Trendelicious indicator

We go long when an uptrend started 2 candles ago.

We close the position when an uptrend ended 2 candles ago.

Parameters are just the required parameters for the indicator + backtest timeframe

To avoid the noise and catch big uptrends, run on higher timeframes (4h, 1D ...)

The script also contains a code to show some stats suitable when on a mobile device.

DISCLAIMER:

This is not an advice to trade. Use at your own risk.

The author of this script cannot be held responsible for any losses incurred directly or indirectly by the usage of this strategy.

Ultimate Ichimoku Cloud StrategyThe goal of this strategy script is to provide the ultimate experience to anyone interested in the Ichimoku Kinkō Hyō (Ichimoku Cloud). The script is designed to be highly customizable and allows the user to set a custom trade date range and select any combination of inputs and conditions that satisfy their goals. Additionally, the script allows the user to visually see any combination of their set conditions by clicking the " Show Conditions Visually " checkbox. Doing so will color the background in a different color where the conditions align. Finally, a simple Stop/Take profit is added for those that wish to exit based on percentages over Ichimoku conditions.

As always, please let me know if there are any bugs, something useful that could be added or if you need some help. Leave a like if you wish!

TENKAN BOLTTENKAN BOLT

7 major point in this indicator are as follows :-

•Tenkan-sen

•Ichimoku Cloud

•Exponential Moving Average

•Change of Volume Analysis (calculated in background)

•Modified Keltner Channel (calculated in background)

•RSI Divergence (calculated in background)

•Entry and Exit Point

www.tradingview.com

There will be 2 types of Long entry alert and 2 types of Short entry alert.

•The first one is marked as "Long" or "Short" only which indicates the signal calculated by Keltner Channel, Tenkan-sen and change of volume in sudden time.

•The second one is marked as "Long Divergence" and "Short Divergence" which indicates signal by RSI Divergence in my own way (not aggressive).

The idea of this script is only trade the highest probability setup and I shall call it the "High Probability, Probability Trading". This is definitely not a buy or sell call as the idea of the script is to give a good direction for trader and to learn the high probability trading setup which includes the volatility of the market.

This script specifically created for Futures Crude Palm OIL (FCPO) market and may works differently in different market. It works great in 1 minute time-frame and 3 minute time-frame

(with slight adjustment).

Kindly contact me for usage. Thanks!

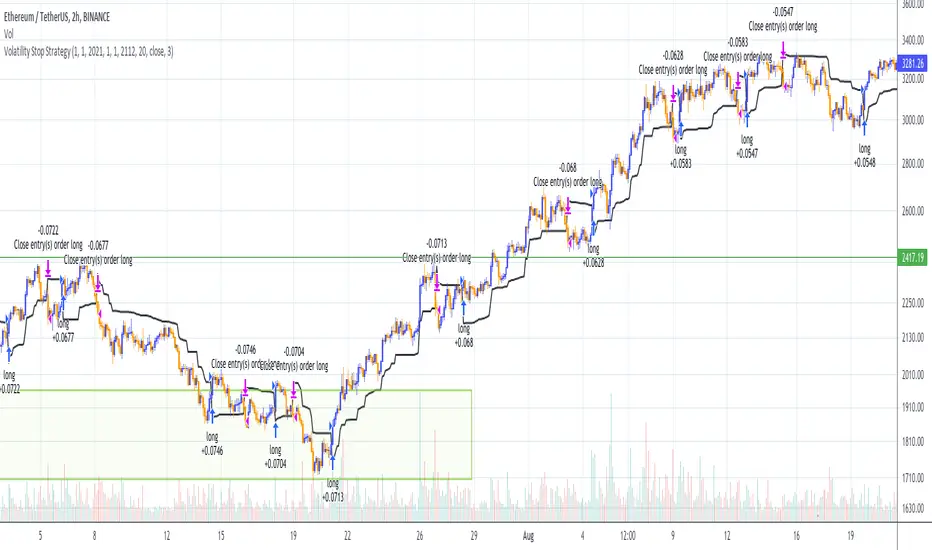

Volatility Stop Strategy (by Coinrule)Traders often use the volatility stop to protect trades dynamically, adjusting the stop price gradually based on the asset's volatility.

Just like the volatility stop is a great way to capture trend reversals on the downside, the opposite applies as well. Therefore, another useful application of the volatility stop is to add it to a trading system to signal potential trend reversals to catch a good buy opportunity.

ENTRY

- When the price crosses above the Volatility Stop

EXIT

- When the price crosses below the Volatility Stop

For this strategy, the Volatility stop's multiplier is set to 3 to allow more flexibility to the trade. The strategy is designed for medium-term trades.

Based on the backtest result from a sample of crypto trading pairs, the most profitable time frame is the 2-hr.

The strategy works well with both crypto-to-crypto and crypto-to-fiat pairs. To make results more realistic, a trading fee of 0.1% is added to the script. The fee is aligned to the base fee applied on Binance.

Bagheri IG Ether v2In this version, the winning ratio has been decreased, but the Risk to Reward Ratio (RRR) has been set to be better than the previous version.

This is a technical trading strategy for Ethereum ( BINANCE:ETHUSDT ). We built and developed it on MetaEditor and optimized it with MetaTrader optimizer.

The main indicators are Donchian Channel, Oscillator of ROC , Bears Power, Balance of Power , and Simple Moving Average ( SMA ). Default values in the input panel are the best combination of these indicators, but you can change any of them and try it for better results.

Please notice that this strategy has been optimized on the 1-minute chart of Ethereum .

For each position, you can see the Take Profit (TP) and Stop Loss (SL) levels. Also, you can find the values of mentioned TP and SL in points from the input panel of the script.

Attention: The price of Ethereum has 2 decimal places.

Therefore, 3000 points for TP means 30 USDT for trading 1 BINANCE:ETHUSDT .

Bagheri IG EtherThis is a technical trading strategy for Ethereum ( BINANCE:ETHUSDT ). We built and developed it on MetaEditor and optimized it with MetaTrader optimizer.

The main indicators are Donchian Channel, Oscillator of ROC, Bears Power, Balance of Power, and Simple Moving Average (SMA). Default values in the input panel are the best combination of these indicators, but you can change any of them and try it for better results.

Please notice that this strategy has been optimized on the 1-minute chart of Ethereum.

For each position, you can see the Take Profit (TP) and Stop Loss (SL) levels. Also, you can find the values of mentioned TP and SL in points from the input panel of the script.

Attention: The price of Ethereum has 2 decimal places.

Therefore, 3000 points for TP means 30 USDT for trading 1 BINANCE:ETHUSDT .

Donchian Channels Trending Breakout StrategyThis script looks for two entry signals. Long is when the previous breakout of the donchian channels was a low, price is above the input EMA, current price is equal or higher than the upper band and we're not in a position yet. Short is the other way around, so previous breakout of the donchian channels was a high, price is below the input EMA, current price is equal or lower than the lower band.

I haven't found a script that does take the previous highs and lows into consideration. Works for any markets in any conditions because the stop loss and profit targets are based on the upper and lower band of the donchian channels, which means the stop loss and profit targets move with the trend.

For more details see the script itself, I wrote a ton of comments.

SNAP BACK 2.0 Strategy

This strategy is designed to allow you to catch the bounce or "SNAP Back" of an equity that has been in a trend.

1) Once the moving averages are in the order of 200SMA > 50 SMA > 34EMA > 20SMA > 8EMA (or reverse for and uptrend), the strategy is setup.

2) Next you wait for a trigger of the closing price crossing the 8EMA, while there is a desired gap size between the 8EMA and the 20SMA (2-10% of stock value preferred).

3) Exit position based on target profit reached (conservative sell half at 34EMA and engage a trailing stop loss for remainder or set static limit) or price crosses 8EMA or stop loss%

*)This code also allows you to determine your desired backtesting date compliments of alanaster

This code is the product of many hours of hard work on the part of the greater tradingview community. The credit goes to everyone in the community who has put code out there for the greater good.

The idea for the coding came from a video I watched on YouTube presented by TradeStation called Snap Back - thank you guys for the inspiration.

UPDATE: I have coded the other side of the strategy to allow you to take advantage of the same set-up in an uptrend for Short plays. You can turn the up or downsides on, off, or both.

The main intent is to catch the bounces of a falling stock. However, I have found that you can do the inverse and catch the drops in a rising stock (the latter is not as reliable). This also tends to work better on less volatile stocks. I have included a large volume of user defined conditions and display entry and exit conditions on the chart to see how your choices are impacting the script.

Simple RSI strategyso this script just take it as teaching how to make easy strategy

many time we try complex one and we fail

thanks to coinrule for his very smart method of pyramid

i just here in this very simple rsi strategy want to show how even lame strategy like RSI can be very profitable:)

1. we exit by take profit

2. we make sure that for exit by take profit the stop loss will be far lets say 10% or more

3. this shit only work good in up trending markets:)

why regular rsi strategy not working? because the exit is shity ... it depend on false top that based on RSI above 70 or 80 in general.

in bullish state this will exit us faster then we desire and will cost us loss . in bearish state rsi will not go so high and we exit too late so the stop loss is our our only saver

here by exiting by% we get much better results

so what happen if the trend is bearish? you can can try to do the same just reverse order to create more shorts (sometime it work sometime is not)

end conclusion in bullish trending market even shifty strategy is good

the only reason this one work is actually because of the script of coinrule so i want to thank him on this

happy new year to all TV members

RSI of Ultimate Oscillator [SHORT Selling] StrategyThis is SHORT selling strategy with Ultimate Oscillator. Instead of drectly using the UO oscillator , I have used RSI on UO (as I did in my previous strategies )

Ultimator Oscillator settings are 5, 10 and 15

RSI of UO setting is 5

Short Sell

==========

I have used moving averages from WilliamAlligator indicator --- settings are 10(Lips), 20(teeth) and 50 (Jaw)

when Lips , Teeth and Jaw are aligned to downtrend (that means Lips < Teeth < Jaw )

Look for RSIofUO dropping below 60 ( setting parameter is Sell Line )

Partial Exit

==========

When RSIofUO crossing up Oversold line i.e 30

Cover Short / Exit

=================

When RSIofUO crosisng above overbought line i.e 70

StopLoss

========

StopLoss defaulted to 3 % , Though it is mentioned in settings , it has not been not used to calcuate and StopLoss Exit... Reason is, when RSIofUO already crossed 60 line (for SHORTING) , then it would take more efforts go up beynd 60. There is saying price takes stairs to climb up but it takes elevator to go down. I have not purely depend on this to exit stop loss, however noticed the trades in this stratgey did not get out with loss higher than when RSIofUO reaching 70 level.

Note

======

Williams Alligator is not drawn from the script. It is manually added to chart for illustration purpose. Please add it when you are using this strategy , whch woould give an idea how the strategy is taking Short Trades.

This is tested on Hourly chart for SPY

Bar color changes to purple when the strategy is in SHORT trade

Warning

========

For the eductional purposes only

Weighted Price Oscillator (STRATEGY)Weighted Price Oscillator is an unique indicator that shows the relationship between two custom variables that trigger signals upon specific conditions. When WPO (short for weighted price oscillator) crosses over the signal or zero line, it creates a buy signal and conversely below the signal or zero line, it generates a take profit signal. All of which are provided that the specific conditions are met.

Inside the script's options, the following options are: signal sensitivity, enable signal background color, and take profit percentage. The signal sensitivity allows you to adjust the script's trigger sensitivity, so that the script can fire signals appropriate for a specific timeframe. Enabling signal background color will provide a visual on the oscillator when a buy or take profit signal is being created. And lastly, the take profit percentage option is for configuring the trade size percentage of which you want to take profit with.

PM me for access.

Donchian Channel Strategy [for free bot]

I present to you a script for testing the Donchian channel breakout strategy for the Binance_exchange.

This strategy is trending, and is especially effective for trading cryptocurrency futures.

This strategy is very flexible, and you can configure virtually all possible parameters, moreover, separately for longs and separately for shorts.

In the script, you can configure the parameters of the channel for entry and exit, the exit method, enable or disable purchases / sales, specify take profit and stop loss, and more.

On the example of optimization, only 20% of the deposit is used. This is done for diversification, since there are 37 contracts on binance_futures (at the time of writing the script description). That is, by optimizing the parameters for different currencies, you can very well reduce risks.

Представляю Вам скрипт для тестирования стратегии пробоя канала Дончиана для биржи Бинанс.

Данная стратегия относится к трендовым, и особенно эффективная на торговли криптовалютных фьючерсов.

Данная стратегия очень гибкая, и можно настроить фактически все возможные параметры, при чем, отдельно для покупок и отдельно для продаж.

В скрипте можно настроить параметры канала на вход и на выход, метод выхода, разрешить или запретить покупки/проаджи, указать тейк-профит и стоп-лосс и другое.

На примере оптимизации используется всего 20% от депозита. Это сделано для диверсификации, так как на фьючерсах бинансе присутсвует 37 контрактов (на момент написания описания скрипта). Т.е., оптимизировав параметры под разные валюты, можно очень хорошо снизить риски.

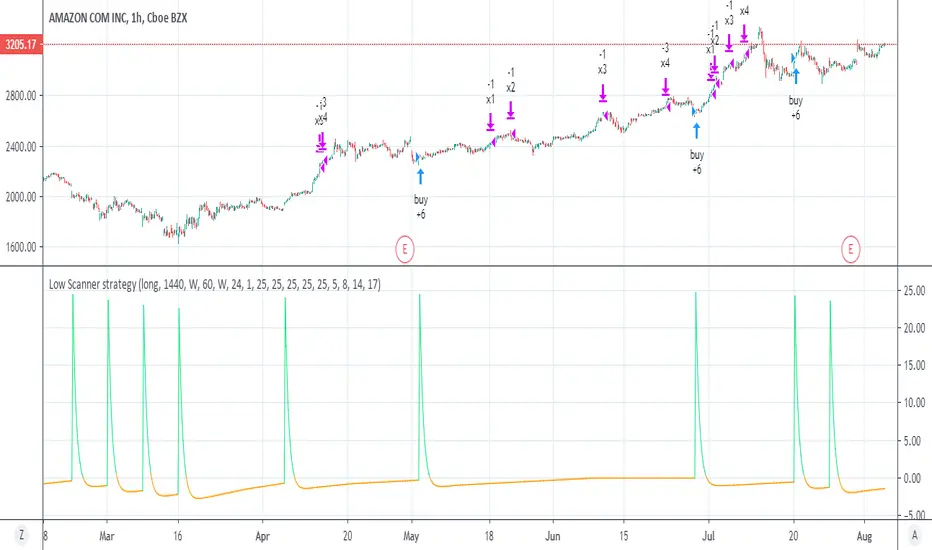

Low Scanner strategyThis is the strategy I made using low scanner

there is no repaint as there is no security at all

the exit is by using multiple exit point by equity shown in the script of adolgov

so you can set the low low scanner to any position you want by no security MTF (look on the study for detail about it)

the exit you set acording to % and the equity as suggested by adolgov

this scripyt is free you can make the exit diiferent

it just example how to create better non repainting strategies with MTF

look on the same setting on stocks just 1 hour candle look very nice there:)

ADX_TSI_Bol Band Trend ChaserThe idea of this script is to be a low risk strategy on trending stocks (or any other trending market), aiming to achieve minimal draw down (e.g. at time of writing AAPL only had ~1.36% draw down, FB ~1.93% draw down and the SPY was 0.80% draw down and all remained profitable).

Testing proved it shouldn't be used in choppy stocks and best period was on daily charts. The back test filter goes back until 2010 so you can obtain 10 years of data.

The strategy utilizes the 200 Moving Average, a Custom Bollinger Band, a TSI with 52 period weighted moving average and ADX strength.

Although back test dates are set to 2010 - 2020, all other filters (moving average, ADX, TSI , Bollinger Band) are not locked so they can be user amended if desired. However the current settings have been tested with manual trading for quite some time to get this combination correct.

Buy signal is given when trading above the 200 moving average + 5 candles have closed above the upper custom Bollinger + the TSI is positive + ADX is above 20.

As back testing proved that this traded better only in tends then some Sell/Short conditions have been removed from the script and this only takes Long orders.

Only requires 2 additional lines of code to add shorting order and then remove the "buy" condition and this could be used for a downward trending stock instead.

Close for either long or short trades is signaled once the TSI crosses in the opposite direction indicating change in trend strength.

Further optimization could be achieved by adding a stop loss, which I may do in the future.

NOTE: This only shows the lower indicators however for visualization you can use my script "CUSTOM BOLLINGER WITH SMA", which is the upper indicators in this strategy.

This is my first attempt at coding a strategy so I'm happy to receive any feedback or hints on how this could be written better from any experienced coders!

NASDAQ:AAPL AMEX:SPY

Volume Based Buy/SellThis is my very first scrip on this platform. It's the first version of the script, It works on the volume-based moving averages and exponential moving average.

I have added the buy/sell signals for educational purposes only. While adding the buy/sell signal I have an additional check on the strength of the trend to reduce loss to a minimum.

How to use:

1. Use with Heikin Ashi Chart.

2. Use 15 Min timeframe for intraday.

Some improvements I am working in the near future is:

1. Exit tread with the maximum profit.

2. Reduce down false trad to 0%.

To encourage and support please like the script try using for your own paper trading.

Dont forget to leave a comment on if you see any improvement in the script or any idea you have. Happy treading together.

XProfit Strategy BacktesterHello,

This Script is a Backtesting Strategy tester of XProfit and allows users to clearly define a profitable strategy.

To Define a profitable strategy, there is the option to modify the parameters "XR" and "Sensitivity".

The Script in itself is build on ATR which gives Long or Short signal.

Note: The strategy script does not allow alerts. It does only allow backtesting.

How To Get Access: DM me for a Trial or use the links below this post to purchase the Indicator which will automatically come with XProfit

Happy Trading.

GoldMode On (Triple compromise strategy) TF 60-240BINANCE:BTCUSDT

Greetings.

I am publishing this script in order to get feedback for further work on it.

The script combines a compromise between several classic strategies, and each of them uses modifications of classic indicators on specially selected averaging sliding indicators.

1. The script uses an ATR-based filter (it's off by default, as it's better on BTCUSD , but you can enable it in the settings if you want to use it on EURUSD , for example, or on other symbols).

2. A strategy based on crossing the moving.

3. A strategy based on determining the direction of movement of the modified slow and fast RSI .

4. A strategy based on the modified ADX +DI -DI .

The essence of the strategy in finding a compromise decision on the signals coming from each of these three strategies.

=====

Приветствую.

Данный скрипт публикую с целью получить обратную связь для дальнейшей работы над ним.

Скрипт сочетает в себе компромисс между несколькими классическими стратегиями, причём каждая из них использует модификации классических индикаторов на специальным образом подобранные усредняющие скользящие.

1. В скрипте используется фильтр на основе ATR (по умолчанию выключен, т.к. на BTCUSD так лучше, но можно включить в настройках, если хотите использовать его на EURUSD , например, или на других инструментах).

2. Стратегия основанная на пересечении скользящих.

3. Стратегия основанная на определении направления движения модифицированных медленной и быстрой RSI .

4. Стратегия основанная на модифицированном ADX +DI -DI .

Суть стратегии в поиске компромиссного принятия решения по сигналам поступающим от каждой из этих трёх стратегий.